You have $10 million to invest.

Would you bet on the next big startup—a risky but potentially explosive venture—or put your money into a stable, established company, fine-tuning operations for steady gains?

That’s the fundamental breaking point between Venture Capital (VC) vs. Private Equity (PE).

VC is all about high-growth startups, banking on the next unicorn. PE, on the other hand, buys into mature businesses, optimizing them for long-term profits.

According to S&P Global Market Intelligence, global private equity and venture capital transactions reached $35.28 billion in January, showing a slight decline compared to the same period in 2024.

Source: Spglobal

So, which strategy actually delivers the biggest returns?

A Private Equity Firm Marketing Agency will define success differently from a Venture Capital-backed tech startup, stating that one thrives on high risk and high reward, while the other banks on predictable value creation.

But when it comes to real investor profits, is it better to chase the moon or play it smart?

Let’s break down the numbers, the risks, and the biggest wins to see which model truly dominates the ROI game.

Private Equity: The Power Players of Business

What is private equity? Firstly, know that Private equity (PE) firms don’t gamble on ideas—they invest in established companies with predictable cash flows.

Instead of betting on the next big thing, they buy businesses, restructure them, and sell for profit. Think of it as flipping houses but on a corporate scale.

How PE Firms Make Money

- Buy: PE firms acquire majority stakes or entire companies, often struggling businesses or undervalued firms.

- Restructure: They cut costs, improve operations, and boost profitability—making the business leaner and more valuable.

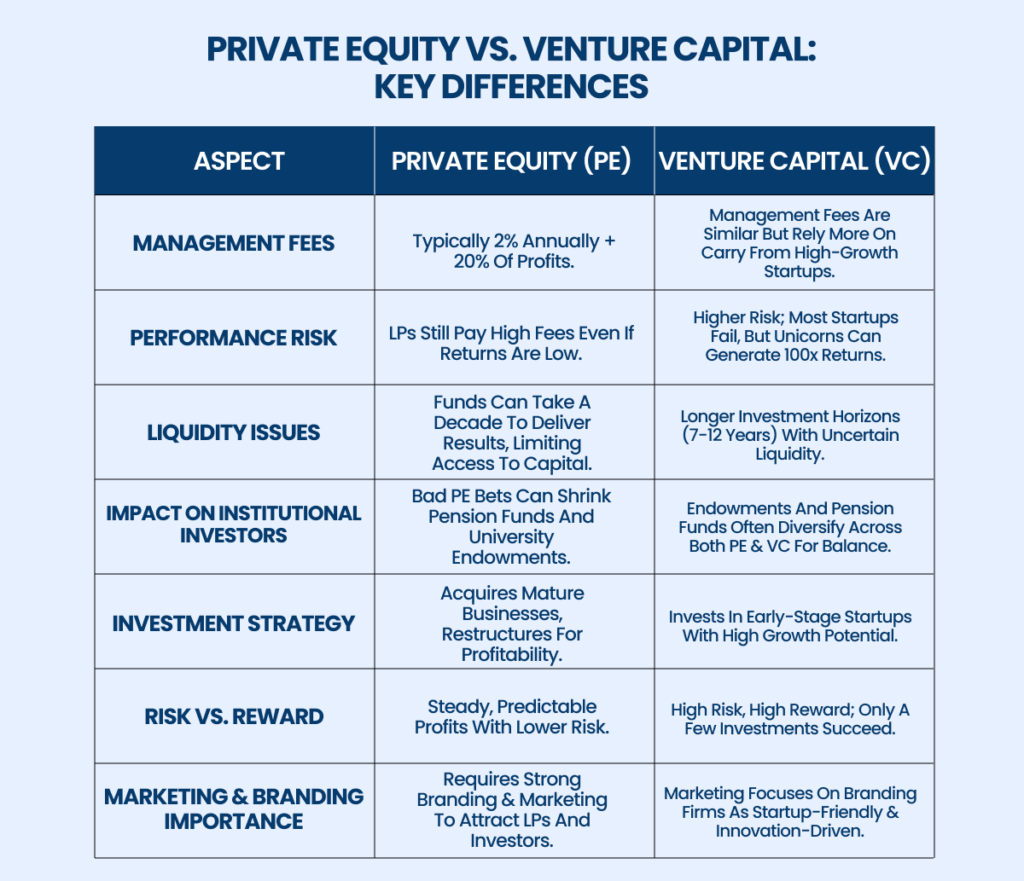

- Sell: After 5-7 years, the firm exits—either through selling to another company, an IPO, or a secondary buyout.

The Secret: Leveraged Buyouts (LBOs) and Operational Improvements

One of PE’s biggest tools is the leveraged buyout (LBO)—where firms use a mix of debt and equity to acquire a company.

Instead of using all their own cash, PE firms take loans secured against the company’s assets, allowing them to own more for less upfront investment.

But PE isn’t just about financial maneuvering.

The real value comes from operational improvements:

- Cost-cutting: Trimming inefficiencies, renegotiating supplier contracts.

- Management restructuring: Bringing in experienced executives to drive performance.

- Expanding revenue streams: Scaling products, entering new markets.

Stable Businesses vs. Disruptive Innovation

Unlike venture capital, which thrives on fast-growing startups, PE firms look for predictable revenue and stable cash flows.

They focus on industries like:

- Fintech SaaS (acquiring profitable software businesses with recurring revenue).

- Home Services (buying HVAC, plumbing, and roofing companies with strong local demand).

- E-Commerce (acquiring direct-to-consumer brands with steady customer bases).

PE firms aren’t looking for moonshots—they want reliable, steady returns with controlled risks.

Venture Capital: The Startup Dream Machine

Venture capital (VC) is built on high-risk, high-reward bets.

Instead of acquiring mature companies, VCs inject capital into early-stage startups, hoping they become the next Stripe, Airbnb, or OpenAI.

How VC Bets on High-Growth Startups

VC firms don’t buy companies outright. Instead, they invest small amounts across multiple startups, taking minority stakes in exchange for funding.

They bank on the idea that one or two big successes will cover the losses from others that fail.

Unlike PE, VC returns aren’t about fixing companies—they’re about scaling fast:

- Funding product development: From MVP to full-scale launch.

- Expanding user acquisition: Helping startups grow their customer base rapidly.

- Securing follow-up investments: Taking startups through Series A, B, C rounds until IPO or acquisition.

The Winner-Takes-All Model: A Few Big Wins Pay for Many Losses

The math behind VC is brutal—most startups fail within five years. But when a startup succeeds, it can return 100x or more.

- Sequoia Capital’s investment in WhatsApp ($60M) turned into $3B when Facebook acquired it.

- Andreessen Horowitz put $250M into Airbnb, now worth over $80B.

These massive wins compensate for the countless startups that never make it.

The Role of Angel Investors, Accelerators, and Series A/B Funding

Before VCs step in, angel investors and accelerators help fund the earliest stages.

Programs like Y Combinator take raw ideas and help shape them into investment-ready businesses.

Once a startup gains traction, it moves through funding rounds:

- Seed funding – Early-stage capital for market validation.

- Series A & B – Focused on user growth and revenue scaling.

- Series C and beyond – Aiming for IPOs or acquisitions.

Unlike PE, where returns come from operational improvements, VC wins depend on market growth and investor sentiment.

Show Me the Money: Which Model Delivers the Biggest Returns?

When it comes to returns, PE and VC operate on different expectations.

PE focuses on steady, risk-adjusted gains, while VC swings for the fences.

10-Year IRR Comparison: Private Equity vs. Venture Capital

According to Cambridge Associates:

- Private Equity: 13-15% annualized returns.

- Venture Capital: 11-12% annualized returns (but with higher variance).

While PE typically delivers more consistent profits, VC has outlier successes that can return 50-100x.

Why Some VC Firms Achieve 100x Returns While Others Crash

VC success is heavily dependent on the market cycle.

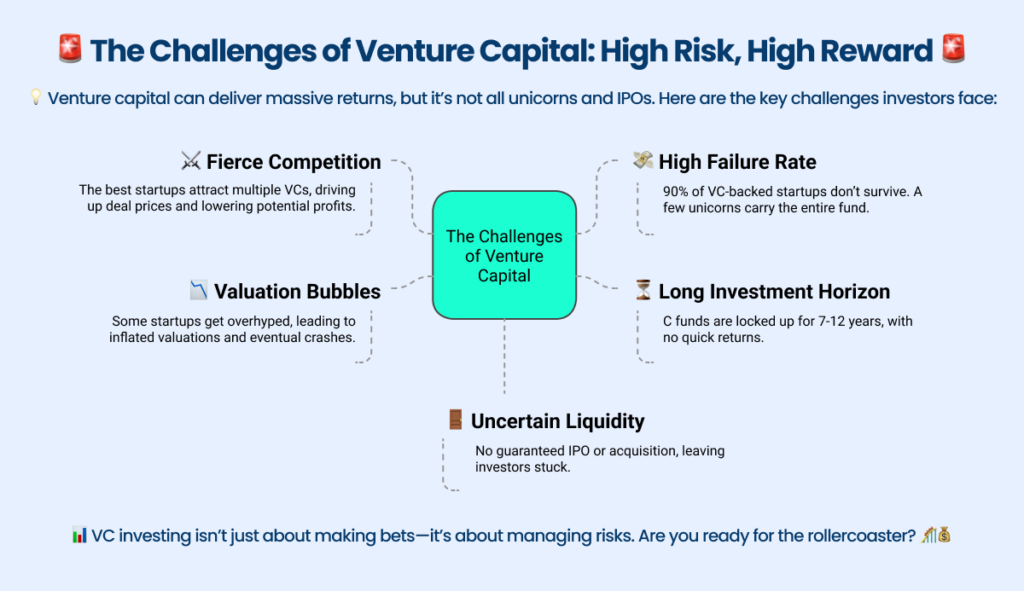

During boom periods, valuations skyrocket. But when markets dip, startup funding dries up.

- In 2022, global VC funding fell by 35% as interest rates rose.

- Only 1 in 10 startups reach Series C funding.

PE, by contrast, is less vulnerable to hype cycles. Even in recessions, established businesses generate revenue, making PE more resilient in downturns.

Risk vs. Reward: The Dark Side of Both Models

Every investment comes with risks, but private equity vs. venture capital presents two completely different kinds of challenges.

Venture capital bets on big ideas and high-risk startups, while private equity takes on established businesses with financial engineering tactics.

When private equity marketing strategies go wrong, they don’t just fail quietly—they can implode spectacularly, leaving investors, employees, and entire industries in turmoil.

The VC Gamble: Is It Worth the Hype?

Venture capital thrives on disrupting industries, but the reality is that most startups don’t make it past five years.

Investors know this, yet they keep pouring billions into early-stage companies, hoping to strike gold.

90% of VC-backed Startups Fail—What Happens to Investors?

According to Harvard Business School, 75% of VC-backed startups never return capital to investors.

When a startup folds, venture capitalists don’t just lose money—they also lose years of funding, mentorship, and strategic planning.

VC firms expect most investments to fail, which is why they follow the unicorn strategy—the idea that one massive success can offset a portfolio full of losses.

The Biggest VC Disasters: WeWork, Theranos & Overhyped Flops

Some VC-backed companies grow fast but collapse even faster.

Take WeWork, which once had a $47 billion valuation before plummeting to under $3 billion. Investors, including SoftBank, lost billions when WeWork’s business model failed to match its hype.

Then there’s Theranos, the health-tech company that promised to change blood testing but instead delivered one of the biggest fraud scandals in VC history. Investors, including the Walton family and Rupert Murdoch, lost over $900 million.

Why VCs Rely on the “Unicorn Strategy” (1 in 10 Investments Succeeds)

Venture capital operates like a lottery for billionaires. If one company reaches IPO or gets acquired, it can return 50-100x the original investment.

That’s why VC firms like Sequoia Capital and Andreessen Horowitz make hundreds of investments per year—they only need one Airbnb, Stripe, or Shopify to make it all worthwhile.

But for every unicorn, dozens of well-funded startups disappear without a trace.

When PE Goes Wrong: The Leveraged Buyout Trap

Private equity firms focus on buying and restructuring mature businesses, but when deals go wrong, they can sink entire companies under mountains of debt.

How Debt-Fueled PE Deals Can Bankrupt Companies (e.g., Toys “R” Us)

Private equity often acquires companies using leveraged buyouts (LBOs)—meaning they borrow massive amounts of money to fund the purchase.

The problem? If the acquired company fails to generate enough cash flow, it drowns in debt.

That’s exactly what happened to Toys “R” Us. After being acquired by PE firms KKR, Bain Capital, and Vornado in 2005 for $6.6 billion, the company couldn’t keep up with interest payments. By 2017, it collapsed under its debt load, shutting down 800 stores and leaving 30,000 employees jobless.

Why Overleveraging Destroys Businesses and Jobs

PE firms often cut costs aggressively to boost short-term profits, but this can cripple long-term growth.

When PE firms load a company with debt, slash jobs, and strip assets, they may make a quick profit but leave a hollowed-out business behind.

Industries most vulnerable to PE takeovers include:

- Retail (Sears, Payless Shoes, J.Crew)

- Healthcare (Hahnemann University Hospital in Philadelphia was forced to shut down after a PE acquisition)

- Media (Sports Illustrated struggled after a PE buyout led to cost cuts and layoffs)

The Hidden Risks of High-Fee PE Funds for Investors

PE funds charge high management fees (typically 2% annually plus 20% of profits).

But if the fund underperforms, LPs (limited partners) still pay high fees, even if their returns are mediocre. Some funds take a decade to show results, tying up investor capital for years without liquidity.

For pension funds and endowments, bad PE bets can shrink retirement accounts and university funds—making PE’s risk far more than just a corporate issue.

Final Verdict: Where Should Your Money Go?

Private equity and venture capital follow two completely different playbooks, but they share one common goal: delivering high returns. If you want steady, predictable profits, private equity is the safer bet, while venture capital is high risk, high reward.

[A] Growth Agency will help investors, fund managers, and business owners navigate both models effectively. Whether you’re a PE firm looking to attract institutional investors or a VC-backed startup trying to stand out, the right private equity marketing strategies and venture capital branding can make all the difference. We promise you to succeed in the process.

We craft data-driven strategies that position PE firms in front of the right investors, ensuring funds are recognized, trusted, and funded.

Our expertise ensures that your firm doesn’t just compete—it dominates. With a deep understanding of private markets, fintech, SaaS, and e-commerce, we craft marketing strategies that directly impact investor trust and funding success.