In the digital age, neobanks are reshaping the landscape of financial services.

Emerging in the early 2000s, over a decade ago, these fintech-forward alternatives challenge traditional or online banks by prioritizing cutting-edge technology to streamline customer experiences, slash costs, and broaden online access to financial services without operating any physical branch.

The tumult of the 2008 financial crisis cast a long shadow over traditional banks, fueling a surge in demand for more transparent and innovative financial solutions.

(source)

As smartphones became ubiquitous in the early 2010s, neobanks seized the moment, harnessing mobile technology to meet the growing consumer appetite for managing finances at a tap. Now, the value of transactions is projected to increase at an annual growth rate (CAGR) of 13.15% from 2024 to 2028, reaching a total of US$10.44 trillion by 2028.

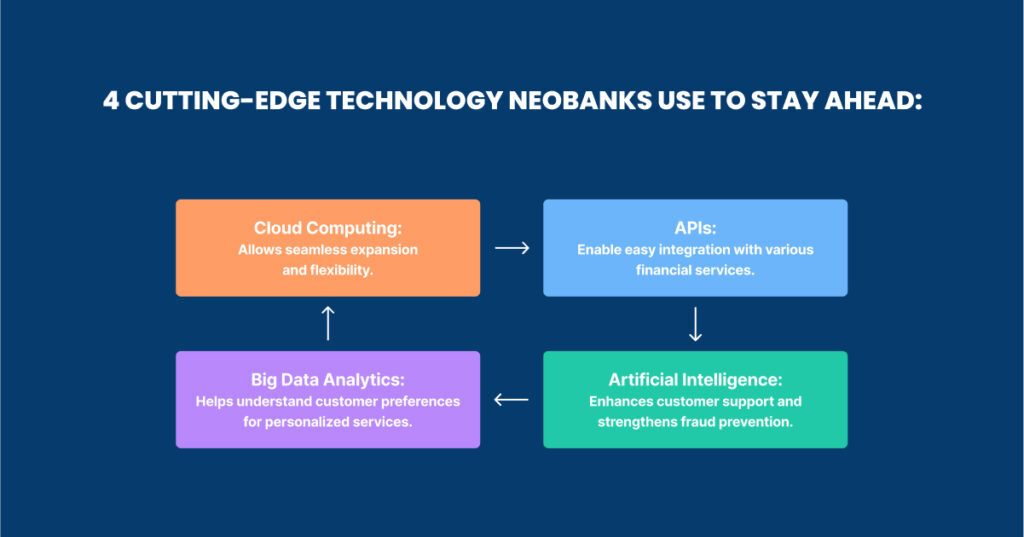

Inside the Tech of Neobanks

At the core of neobanks lies a sophisticated tech framework that propels their innovative edge:

- Cloud Computing: Offers the elasticity and agility to scale operations seamlessly.

- APIs: Create a web of connectivity, enabling smooth integrations with diverse financial platforms.

- Big Data Analytics: Provides insights into customer preferences and behaviors, tailoring personalized banking experiences.

- Artificial Intelligence: Powers advanced customer support and robust fraud detection mechanisms.

This technological foundation fuels their rapid growth and defines a new frontier in banking where convenience, efficiency, and accessibility are paramount.

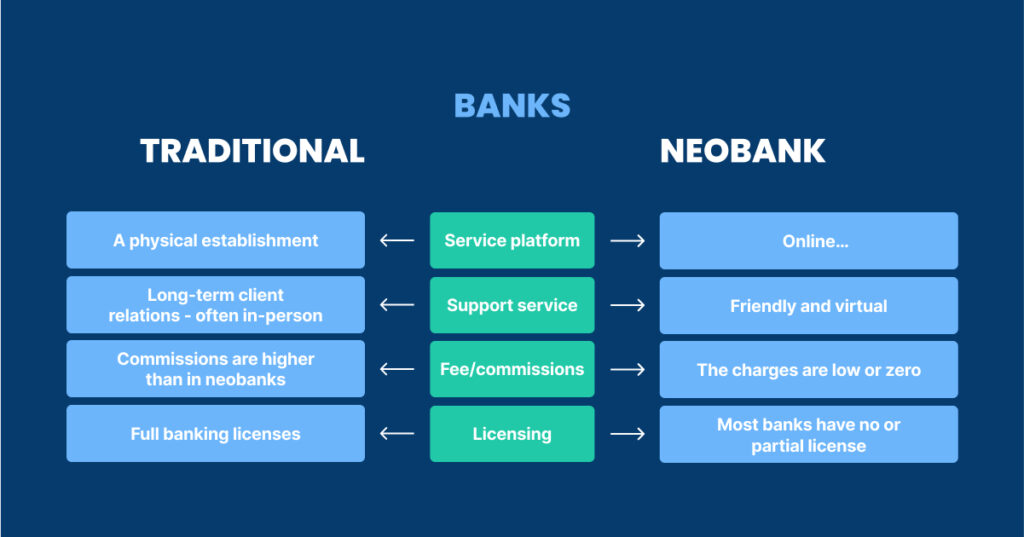

Key Features That Distinguish Neobanks from Traditional Banks

App-based services: Neobanks offer services through mobile apps, including account management, money transfers, and tools for budgeting.

Real-time updates: Account holders receive instant notifications and updates on their transactions and account changes, a significant improvement over traditional bank processing times.

Discussion of API-Driven Banking and Its Implications for Service Agility and Customer Interaction

API-driven banking is at the core of neobanks’ operational model. It allows these banks to adapt to changes quickly, integrate with various fintech services, and innovate their product offerings without heavy infrastructural changes.

For customers, this means more personalized and responsive services and seamless banking integration into their daily digital activities.

The Business Model of Neobanks

(source)

Neobanks are redefining the financial landscape by leveraging digital-first strategies to provide banking services. Unlike many traditional banks operate without physical branches, significantly reducing overhead costs.

Here’s an exploration of how neobanks generate revenue, their contrast with traditional banking revenue streams, and some successful case studies.

Revenue Generation without Physical Branches

Neobanks utilize several innovative strategies to generate revenue while operating without the traditional brick-and-mortar branches:

Fee-based Revenue: Many neobanks charge fees for premium account features such as higher withdrawal limits, international transactions, or exclusive banking products. These are often structured as annual or monthly subscription fees.

Interchange Fees: Each time a customer uses a neobank’s credit or debit cards, the merchant pays an interchange fee, a portion of which goes to the neobank. This fee typically ranges from 0.7% to 1.5% of the transaction amount.

Third-party Partnerships: Neobanks often partner with other financial service providers and earn commissions by referring their customers to products like insurance, investment accounts and solutions, or loans.

Freemium Models: Many neobanks offer basic bank accounts for free while charging for advanced features, like enhanced financial analytics, budgeting, and savings tools, or artificial intelligence-driven advice.

Contrast with Traditional Banking Revenue Streams

Traditional banks have historically relied on a few primary revenue streams that differ significantly from those of neobanks:

Net Interest Margin: The classic banking model generates most of its revenue through the difference between interest earned on loans and interest paid on deposits. This dependency on interest rates makes traditional banks vulnerable to economic cycles.

Service and Maintenance Fees: Traditional banks often charge fees for account maintenance, ATM use, and other banking services. While neobanks also charge fees, they typically offer more cost-effective solutions due to lower operational costs.

Cross-Selling Financial Products: Although both neobanks and traditional banks engage in this practice, traditional banks have a more extensive portfolio of products they can cross-sell to their existing customer base.

Case Studies of Successful Neobanks

N26 and Revolut are two prominent examples of successful neobanks that have effectively utilized the digital-only business model:

N26: Founded in Germany, N26 has expanded across Europe and into the US, offering transparent, flexible banking solutions.

It generates revenue through a subscription model for premium features, interchange fees, and partnerships with other financial services. N26 has successfully attracted millions of customers by focusing on user-friendly interfaces and minimal fees.

Revolut: Launched in the UK, Revolut offers a range of financial services from currency exchange to cryptocurrency trading.

Besides earning through a subscription model for its premium services, Revolut benefits from interchange fees and a robust approach to offering new products rapidly. Their aggressive expansion into new markets and services has garnered an international customer base.

Regulatory Landscape and Challenges

Neobanks face stringent regulatory environments that demand adherence to financial stability, consumer protection, and anti-money laundering (AML) protocols.

Key considerations also include cybersecurity due to their digital-only model, with different countries imposing varying levels of regulatory oversight.

Challenges in Different Jurisdictions (EU, USA, Asia)

European Union (EU): Neobanks must comply with PSD2 for payment services and GDPR for data protection.

United States (USA): The regulatory framework is complex, with federal and state-level obligations often leading neobanks to partner with traditional banks.

Asia: Regulations vary widely. Places like Singapore and Hong Kong provide digital bank licenses, while India and China maintain stricter controls.

Navigating Regulatory Challenges

Neobanks navigate these challenges through strategies such as:

Partnerships: Many form alliances with established banks to use their licenses and compliance systems.

Compliance Programs: Investment in comprehensive compliance and advanced security and transaction monitoring tech is common.

Regulator Engagement: Proactive engagement with regulatory bodies helps neobanks adapt to and influence financial regulations.

Technology Utilization: They employ cutting-edge technology to meet regulatory demands efficiently.

These strategies help neobanks comply with stringent regulations and actively participate in shaping a more digital-friendly banking regulatory environment.

Recent Innovations and Technological Advances

AI and Machine Learning in Customizing Banking Experiences

Neobanks leverage AI and machine learning to offer personalized banking experiences, enhancing customer service and optimizing operations.

These technologies analyze customer data to predict behaviors, tailor financial advice, automate routine tasks, and enhance security measures through anomaly detection.

Blockchain and Cryptocurrencies in Neobanking

Some neobanks are incorporating blockchain technology and cryptocurrencies into their services. Blockchain offers enhanced transaction security and transparency.

Additionally, by offering cryptocurrency trading and wallets, neobanks cater to a growing market of digital currency users, setting themselves apart from traditional banks.

Customer Acquisition and Market Penetration

Neobanks employ several effective strategies to attract and retain customers, focusing heavily on user experience and digital innovation:

User-Friendly Interfaces: Simplified, intuitive app designs and customer-centric features make banking more accessible and attractive. For example, Monzo offers a seamless sign-up process that can be completed entirely on a smartphone within minutes.

Competitive Pricing: Offering low or no fees for basic banking services and better rates on savings accounts due to lower overhead costs. For instance, Chime charges no overdraft, monthly maintenance, or minimum balance fees.

Customized Products: Leveraging data analytics to offer personalized products and services.

Aggressive Marketing: Utilizing digital marketing channels effectively to reach potential customers, especially on social media platforms where their target demographic is active.

Value-Added Services: Providing additional services like budgeting tools, real-time financial insights, and cryptocurrency transactions, such as Revolut, which integrates cryptocurrency trading directly within its app.

Demographic Analysis of Typical Neobank Users

Typical neobank users are predominantly younger demographics, including millennials and Gen Zers, who are digital natives comfortable with using technology for their financial management.

These users often seek convenience, rapid service, and innovative financial products.

They are also more likely to be engaged with gig economy jobs or freelance work, making the flexibility of neobanks particularly appealing.

Competitive Advantages Over Traditional Banks

Neobanks offer several competitive advantages over traditional banks that help them stand out in the crowded financial services market:

Technological Agility: Ability to quickly adapt to new technologies and integrate innovative solutions faster than traditional banks.

Lower Cost Structure: The absence of physical branches and the associated costs allows neobanks to offer cheaper services.

Rapid Response to Customer Needs: Fast adaptation to customer feedback and agile development cycles ensure that neobanks can quickly roll out needed functionalities or adjustments. For example, N26 regularly updates its app with new features based on user feedback and market research.

Enhanced Data Security: Often built from the ground up with the latest security protocols, providing reassurance to users wary of cyber threats. Starling Bank, for instance, has built a reputation for robust security measures.

Global Accessibility: Easier to set up banking services in multiple jurisdictions, appealing to a global or travel-friendly customer base.

These factors collectively contribute to neobanks’ growing market penetration and appeal to a modern customer base looking for efficient, secure, and user-friendly banking alternatives.

Neobanks: A Look Ahead

(source)

Neobanks, the digital-first financial institutions, are poised for significant growth in the coming years. Here’s a glimpse into their future:

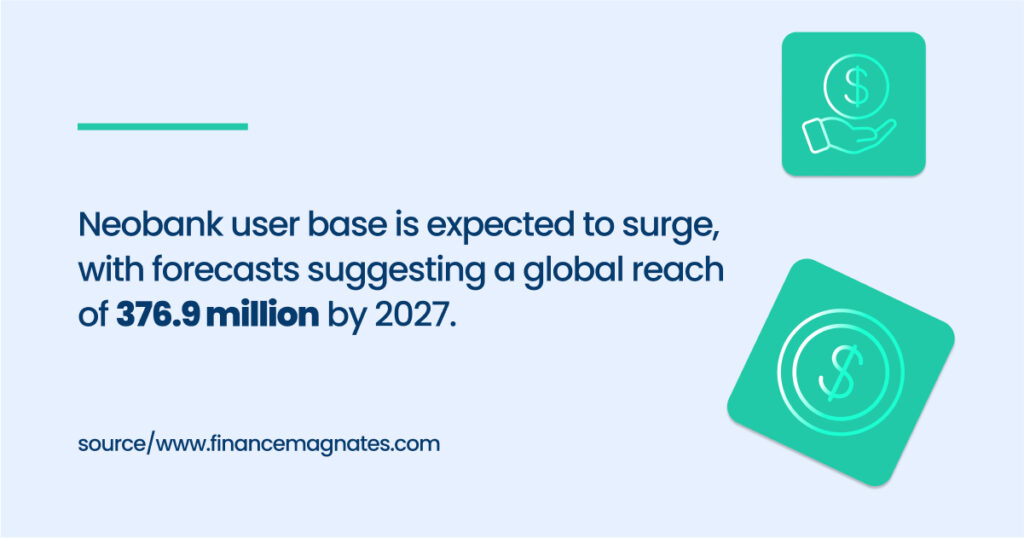

Growth Predictions (5-10 Years):

- Exponential Rise in Users: The user base is expected to surge, with forecasts suggesting a global reach of 376.9 million by 2027. Transaction value is also projected to climb, reaching an estimated $10.44 trillion by 2028.

Market Disruptions and New Entrants:

- Tech Giants as Competitors: Established tech companies like Amazon and Apple may leverage their user base to enter the neobanking space, disrupting the current landscape.

- Niche Specialization: Neobanks might cater to specific demographics or financial needs, offering hyper-personalized services that traditional banks struggle with.

- Increased Consolidation: As players seek wider reach and profitability, mergers and acquisitions within the neobanking sector are likely.

Evolving Role in the Financial Ecosystem:

- Partnerships and Integrations: Collaboration between neobanks and traditional banks or fintech firms is expected to rise, offering a broader range of financial products and services.

- Financial Inclusion: Neobanks can be crucial in bringing unbanked populations into the financial system through their mobile-first approach.

- Focus on Financial Wellness: Neobanks could become hubs for financial management tools, budgeting assistance, and personalized financial advice through AI and machine learning.

Transformative Potential

Neobanks have the potential to reshape the financial landscape by:

Prioritizing User Experience: With their focus on mobile-first interfaces and streamlined processes, they can make banking more user-friendly and accessible.

Promoting Innovation: Neobanks constantly innovate, driving the development of new financial products and services.

FinTech Entrepreneurs: Challenges and Opportunities

The future of neobanking is bright, but challenges remain.

FinTech entrepreneurs need to consider the following:

- Building Profitability: Finding sustainable revenue streams beyond low fees and interest rates will be crucial.

- Regulation and Compliance: Adapting to evolving regulations and ensuring consumer protection will be essential.

Empowering Financial Technology Company with [A] Growth Agency

![Empowering Financial Technology Company with [A] Growth Agency](https://src.azariangrowthagency.com/wp-content/uploads/2024/05/9-9-1024x538.jpg)

Specialized in data-driven marketing and endowed with deep industry insights, [A] Growth Agency provides custom support that turns growth challenges into opportunities.

We offer tailored marketing campaigns specifically designed for fintech needs, ensuring effective customer attraction and retention.

Our advanced analytics and reporting equip fintech partners with critical insights into market trends and consumer behaviors, enabling well-informed strategic decisions.

Through scalable growth strategies, your financial technology company can expand efficiently without compromising quality or customer satisfaction.

Additionally, we facilitate the integration of cutting-edge technologies, such as API-driven banking and blockchain, enhancing service delivery and customer engagement.

Collaborating with [A] Growth Agency accelerates a fintech’s market presence and secures a durable competitive edge crucial for success in the rapidly evolving financial services landscape.