Would you risk half your net worth for a shot at doubling it—knowing there’s a 70% chance of losing it all?

That’s the reality of private market investing when done wrong.

With private market assets hitting $13.1 trillion in 2023, opportunities in private equity, venture capital, and pre-IPO stocks are exploding.

But so are the risks—illiquidity, hidden fees, and misleading valuations trap unprepared investors.

That’s why savvy investors work with an expert Private Markets Agency to access exclusive deals while avoiding costly mistakes.

This guide will show you how to invest in the private market correctly, maximizing gains while minimizing risks.

The “Too Good to Be True” Test – Understanding Risk vs. Reward

Lesson #1 in Private Investing: If it looks like easy money, it’s probably a trap.

Many investors rush into the private market, chasing unicorns, believing they’ve found the next SpaceX or Stripe before the IPO.

The promise? High returns, minimal risk, and an exclusive ticket to wealth.

The reality? Most private investments don’t just fail—they can wipe out capital entirely.

When High Returns Are a Red Flag

Here’s how high-return traps often look:

- A “can’t-miss” pre-IPO deal with “guaranteed” growth.

- A private equity fund promising above-market returns in any economic climate.

- A venture capital opportunity that only takes “smart money” investors but asks for a big upfront check.

Reality Check:

- 90% of startups fail.

- Even successful companies stay illiquid for years, meaning your money is locked up.

- Some “exclusive” deals are overhyped or mispriced—investors who bought into WeWork’s private valuation of $47B learned this the hard way.

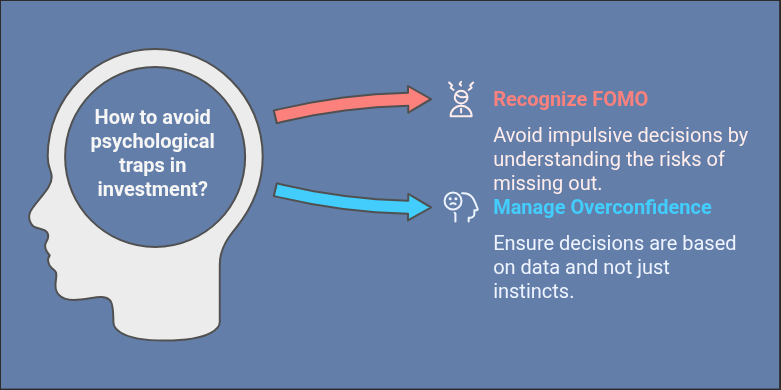

The FOMO & Overconfidence Trap

Two psychological forces make business owners fall for bad private deals:

- FOMO (Fear of Missing Out): “If I don’t invest now, I’ll regret it later.” This rush led investors to pour money into Theranos despite massive red flags.

- Overconfidence: “I have great instincts.” Many early investors in FTX believed they were backing the next financial revolution—until the empire collapsed.

Smart Business Owners Ask:

- Who is selling me this deal, and what’s their track record?

- What happens if I need my money back earlier than expected?

- If this is such a significant investment, why isn’t institutional capital all over it?

The ‘Too Good to Be True’ Test

If an investment promises high returns with no risk, assume it’s a bad deal.

There’s no “guaranteed win” in private markets—only calculated risks with well-planned exits.

The smarter play? Invest where risk is acknowledged, not hidden.

If you’re not hearing about the downside, you’re not getting the whole story.

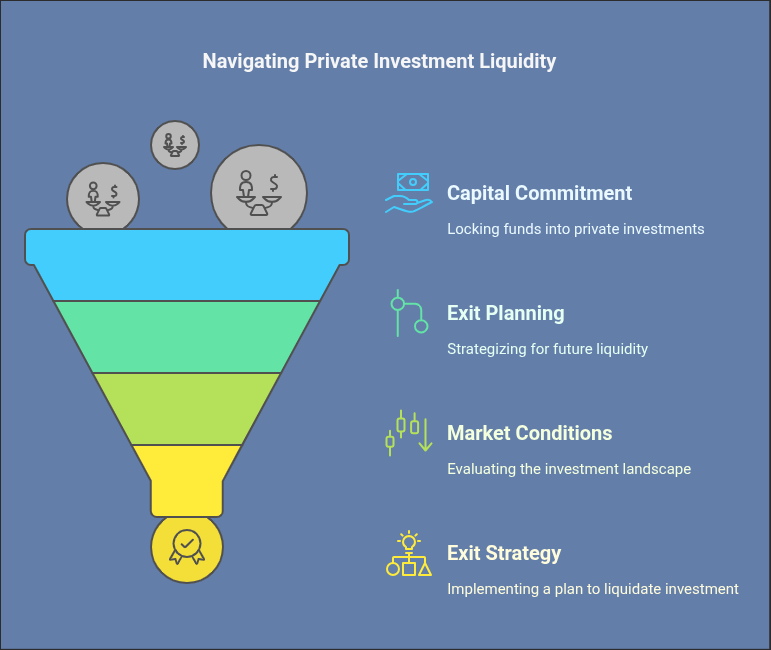

Liquidity is King – Why You Need an Exit Plan Before Entering

Private market investments are easy to get into but hard to get out of—and that’s where many investors go wrong.

Unlike public stocks, where you can sell instantly, private investments often lock up capital for years without guaranteed exit.

The Harsh Reality of Private Market Liquidity

Investors often assume they can sell their private shares whenever they need cash. But in reality:

- Private equity funds have holding periods of 7-10 years before investors see a return.

- Venture capital investments may take a decade or more before a company exits.

- Even in pre-IPO stock markets, selling shares can be challenging due to buyer demand and valuation fluctuations.

Without a clear exit strategy, investors risk being stuck in illiquid assets and unable to cash out when they need it most.

Can Secondary Markets Solve the Liquidity Problem?

Investors try to exit private investments early through secondary markets, where private shares are bought and sold before a company goes public.

Pre-IPO trading platforms like Hiive, Forge, and EquityZen have made this easier by offering a way to sell private stock before an IPO.

But there’s a catch.

The Discount Dilemma – Why Early Exits Come at a Cost

Selling in the secondary market often means taking a steep discount on your investment. For example:

- Due to market volatility, private equity stakes are sold at 30-50% discounts.

- Even promising pre-IPO stocks can sell far below their expected IPO price, depending on market sentiment.

Many investors assume their shares will sell at a premium as a company grows—but that’s rarely the case. When liquidity is tight, buyers set the rules, and desperate sellers take the hit.

TREND: The Rise of Pre-IPO Marketplaces

New platforms like Hiive are making pre-IPO trading more accessible, allowing investors to exit early.

But while these marketplaces provide liquidity, they don’t eliminate the discount problem. Savvy investors use them as a last resort, not a primary exit strategy.

Diversification Done Right – Beyond Just “Not Putting All Eggs in One Basket”

Diversification is a strategic allocation to maximize returns while minimizing risk.

In the private market, where investments are illiquid and high-stakes, inadequate diversification can be just as dangerous as no diversification.

The Danger of Overconcentration

Many investors make the mistake of going all-in on one “big opportunity,” believing they’ve found the next unicorn.

But even high-potential companies fail, and private market investments don’t have the same safety nets as public stocks.

Real-World Example:

- Quibi, the short-form streaming startup, raised $1.75 billion from investors, including high-profile names like Alibaba and JPMorgan.

- The company collapsed in six months, leaving investors with nothing.

How the Pros Diversify in Private Markets

Institutional investors engineer their portfolios with strict risk limits:

- Private equity firms invest in 15-20 companies across multiple sectors to offset risks.

- Venture capitalists balance early-stage startups with later-stage, lower-risk investments.

- Family offices and hedge funds blend private investments with public assets for liquidity.

Finding the Right Balance: Diversification vs. Over-Diversification

Diversifying too much can water down returns, especially in private markets where deal quality varies.

The key is focused diversification—owning a mix of assets without spreading yourself too thin.

DATA: How Much is Too Much?

Industry standards suggest limiting private investment to 10% of your total portfolio to avoid overexposure.

The Deep Dive You Can’t Skip – Mastering Due Diligence

Details are everything.

Private investments rarely have standardized disclosures or audited financials, unlike public stocks, so due diligence is non-negotiable.

Many investors get burned simply because they didn’t ask enough questions early on. Solid due diligence can help you separate legitimate opportunities from costly mistakes.

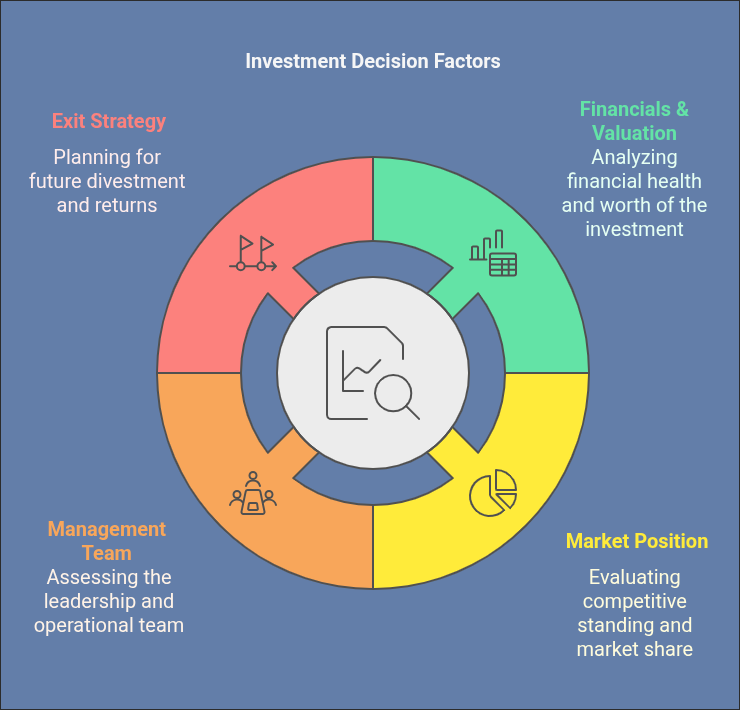

4 Critical Factors to Analyze Before You Write the Check

To invest wisely in the private market, never skip these crucial checks:

1. Financials & Valuation

- Confirm historical performance: revenues, profit margins, and growth rates.

- Evaluate valuation methodology carefully—overinflated valuations are red flags. Remember, Theranos once reached a $9 billion valuation with little verified financial data.

2. Market Position

- Assess the company’s competitive edge: What sets them apart?

- Understand the size and growth of their target market: Is the market sustainable, growing, or saturated?

- Example: Uber disrupted taxis by revolutionizing transportation convenience and efficiency, gaining a clear competitive advantage early on.

3. Management Team

- Evaluate founders’ and leaders’ experience and past track records.

- Check references. Investors who backed WeWork learned a painful lesson about leadership and governance: Chaotic leadership doesn’t always equal good management.

4. Exit Strategy

- Clarify exactly how—and when—you’ll recoup your investment.

- Understand potential liquidity events clearly: IPO, acquisition, secondary sale?

- Don’t invest without clarity here—otherwise, your capital might get locked indefinitely.

The One-Sentence Test

Here’s a quick and powerful hack for evaluating investments:

If you can’t clearly explain how the company makes money in a straightforward sentence, don’t invest.

For example:

- Airbnb connects travelers with affordable short-term accommodations, earning revenue through booking commissions.

- Stripe provides easy-to-integrate payment processing for businesses, generating income through transaction fees.

If you fumble over details, reconsider investing—complicated business models often mask underlying issues.

Avoiding the “Black Hole” – Managing Capital Calls & Illiquidity Risks

One of the most misunderstood aspects of private market investing is the issue of illiquidity—the inability to access your invested capital when you need it most efficiently.

Many business owners underestimate how long their funds could remain tied up, only realizing the depth of this issue when they’re already stuck inside this financial “black hole.”

The Liquidity Trap – Why Your Money is Locked for Years

Unlike publicly traded assets, you can buy and sell freely; private investments often demand long lock-up periods:

- Individual private investments—especially early-stage companies—can remain illiquid for decades.

- Exiting early through secondary markets often means significant discounts (as discussed earlier).

For example, investors in Airbnb waited more than a decade before the company’s IPO provided liquidity.

Capital Calls – The Hidden Commitment

Another key factor investors overlook is the structure of capital calls:

- Most private equity and venture capital funds do not require all your capital upfront.

- Instead, they draw your committed funds gradually (via “capital calls”), typically over the years.

- Failure to meet capital calls can result in severe penalties, including the forfeiture of existing investments in the fund.

This structure requires you to keep liquid cash reserves ready to honor future capital calls, limiting your financial flexibility elsewhere.

Strategies to Maintain Financial Flexibility

Savvy investors carefully balance private and liquid assets to avoid falling into the liquidity trap. Consider these strategies:

- Maintain a Liquidity Reserve

To meet unexpected capital calls, keep at least 20% of your private investment commitments readily accessible in liquid form, such as cash or highly liquid securities. - Use the “Staged Approach” to Private Investing

Spread your private investments gradually over multiple vintages (fund launch years) rather than committing all your capital simultaneously. This ensures regular liquidity events from past investments offset future capital commitments. - Leverage Credit Facilities Responsibly

Some investors use credit lines or lending facilities for temporary liquidity. However, this approach should only be used if interest rates and repayment terms are favorable. Never depend heavily on debt.

Ready to Master How to Invest in the Private Market? Partner with a Private Markets Agency Like [A] Growth Agency

Navigating the private market successfully requires a thoughtful strategy and expert guidance.

Prioritizing proper due diligence, careful liquidity planning, strategic diversification, and deep regulatory awareness are non-negotiables for sustainable, risk-managed growth.

At [A] Growth Agency, we aren’t just another Private Markets Agency—we’re your growth-focused partner, committed to helping you access high-quality private market opportunities while effectively managing risks.

Our data-driven approach ensures that your investment decisions are exciting, innovative, sustainable, and aligned with your long-term financial goals.

Remember: The best investors don’t chase quick wins.

They build sustainable portfolios designed for lasting success. Let’s invest smarter together.